LGB’s Market Commentary for Q4 2023

A Forecast Free Zone

This is the season of forecasts. A bit like midges in the Scottish Highlands, they come around every year, and are about as much use. At the beginning of 2023 these were the forecasts of five major investment firms for the S&P 500 at year end from a starting point of 3,839.5: Barclays 3,675; Morgan Stanley 3,900; UBS 3,900; Citi 3,900 and BlackRock 3,930. The outturn was 4,783 (+24%). And who now remembers the confident and widespread forecasts of Sterling breaking parity with the dollar in Autumn 2022? Certainly not Goldman Sachs who were forecasting 1.30 in December. Forecasting is inherently problematic. Clarity as to where we are now may be as much as we can hope for – and understanding what different classes of investments offer us now, and some of the risks attached, may therefore be useful.

Fixed Income

We can start with the sometimes mislabelled risk-free assets, government bonds. Here is the five-year price chart of the UK 30 year gilt:

(source: FT)

Ouch. With prices having fallen from high to low by well over a half, it is a reminder that lending to governments may mean you get your money back, but your holdings can be subject to massive swings in valuation along the way, particularly for bonds with longer duration.

At the time of writing the UK 10 year gilt are trading somewhere around the middle of their recent range, at a yield to maturity of 3.8%, having hit a high of 4.75% in the autumn, and a low of 3.5% around Christmas. This compares with one month sterling T-Bills yielding 5.15%. US ten year rates hit 5% in October, retreated to just over 3.75% around Christmas and are now at c. 4.05%. Four week US T-Bills yield 5.4%. German 10 Year bonds yield 2.185%, after reaching almost 3% in the autumn and just under 1.9% late last year, whereas short term Euro bills yield around 3.7%. All these markets, with so-called “inverted yield curves” are implying that rates will fall and indeed, inflation does seem to be falling – at least at consumer level (CPI annualised 0.6%, 2.7% in the eurozone and 1.9% for the equivalent US measure). Hence, on the face of it, lending to governments – disregarding of course their regrettable tendency to tax the interest they pay – would seem a reasonable way to safeguard money. And if rates do indeed come down there will be a capital gain as the prices rise.

In the UK, taxpayers can (given the large stock of bonds outstanding issued when rates were much lower) escape much of the tax on interest by buying low-coupon older bonds, government and corporate, which trade on a discount, using the “Qualifying Corporate Bond” exemption: the accretion of the bond to par at maturity is tax free and only the coupon is taxed.

Please note that investors with accounts on the LGB Investments platform have access to UK T-Bills, Gilts and a corporate bond list with suggestions of bonds trading at a discount to par.

However, low CPI, helped down by energy prices in the latter part of 2023, is not the whole story. Central banks (outside the Eurozone) have to worry about the tightness of the labour market, and the danger that inflationary expectations are now baked in. They have seen inflation fall without the recessions they had anticipated but having by common consent waited too long to raise rates, they may well overshoot on the downside. Continued disruption to energy exports, whether from the Gulf via the Red Sea or due to the Ukraine conflict, could reverse the trend. The assumption that current rates are abnormally high is only true if your definition of normality starts with the Global Financial Crisis. But if you believe the inflationary pressures have been vanquished then Gilts and investment grade corporate bonds will offer a reasonable if unexciting return. If normality is indeed a sub 2% rate then longer dated bonds will offer substantial capital gains too. If central banks fail to get inflation down then sub-4% longer term rates do not make much sense.

Investors looking for safe short-term homes for their cash could consider the weekly UK T-Bill auctions. At last week’s auction the 6-month yields were quoted 5.17%-5.21%. Contact us for guidance on how to participate.

There is no consistent way of tracking Sterling sub-investment grade bonds. The US High Yield Bond Index has recovered sharply in the last few months as fears of recession have fallen away and is at an all-time high. Quoted UK high-yield paper has also recovered somewhat (e.g. the Bruntwood 6% 2025 which is trading at 96.5 vs 92.5 in October).

Yields on LGB’s MTN issues have not yet started to fall back and can offer a decent real return in this environment. For example, Lendco Limited, a solid specialist property lender with an outstanding track record and significant private equity backing, is currently offering 11% p.a. for new 2 year notes.

Forecasts for the property market, following some extreme pessimism earlier this year, are now starting to rise (e.g from Pantheon Macroeconomics), and the market continues to be resilient on the back of a 4 million home deficit in the UK, vs. 60,000 build-to-let units in process and total housing unit construction not much over 200,000 per year.

Equities

The US equity market is notoriously dominated by the “Magnificent Seven” tech stocks, which had doubled to mid-December 2023, pulling the rest of the market up (the NASDAQ 100 was up 52% last year, the S&P 24%) – though outside of the seven it was down for the first three quarters of 2023. European markets are the opposite. The UK underperformance (up 1.6% last year) has led to a degree of existential angst but to a large extent reflects the heavy weighting of miners, oil stocks and financials. A recovery of China and a Shell bid for BP (frequently rumoured) would change the statistics somewhat. Smaller stocks have languished and AIM itself has been woeful- it is not yet clear whether the Mansion House reforms will redirect any meaningful amount of pension money into the market, which badly needs some institutional support: small cap and AIM-specialist funds have seen outflows. The consequence has been exaggerated moves on news as market makers try to avoid trouble, and particularly poor performance of companies with clear needs for further funding, whether or not this is for growth or for shoring up balance sheets. The AIM All Share fell almost 10% last year, AIM technology 17%.

Whether a change of government in the UK will make any difference is unclear. On the positive side there have been no stories about ending the Enterprise Investment Scheme (EIS) though IHT relief must be theoretically vulnerable. However illogical the IHT relief on unquoted and AIM stocks might be considered, the effect of removing this for AIM would be dramatic and unpalatable. Influential commentators on the left such as Will Hutton have started calling out the illogicality of a regulatory system which has driven the UK’s pension funds to shun the UK equity market. Changing that will take a while.

We do seem to be seeing some green shoots in AIM and some positive share price reactions to news. But there is no obvious reason for there to be a rebound into sunlight uplands. We continue to focus on restricted areas of the market.

We have seen some evidence of consolidation in AIM as elsewhere, much of it in-industry deals, often backed by private equity but rarely pure PE transactions. The private equity industry is still readjusting to the repricing of debt round the world, and the difficulty of making lucrative exits into public markets- perhaps the institutions have worked out that the bones have often been picked clean by the time the offering comes. As a result, quoted PE vehicles have been trading on perhaps unjustifiably large discounts.

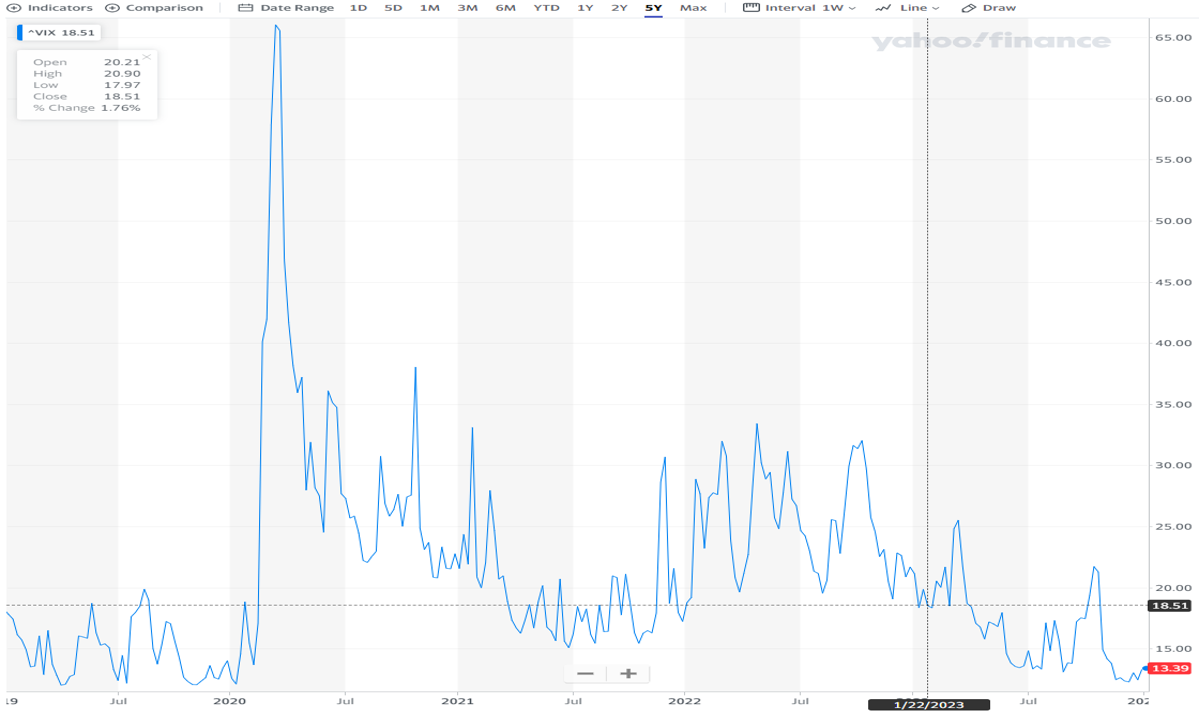

Lastly- in a market ultimately led by the USA, which is intensely inward-looking and arguably becoming more so, it is easy to think that what is going on elsewhere does not matter too much, and that markets are all about economic indicators. Geopolitics matters too. The extended Middle East conflicts- Gaza/Yemen/West Bank/ Lebanon – have the potential at the very least to disrupt the energy markets. Chinese ambitions to seize Taiwan are not going away and arguably look to the day when the US is too self-absorbed to care, but the knock-on effects would be very significant. A Russian victory in the Ukraine – even a ceasefire on current lines – will give the message to Putin that aggression can work, and the temptation to test NATO in the Baltic States at some time in the not too distant future. Volatility on the US VIX measure is more or less at a five-year low – intuitively that does not seem to make sense within the wider context….

Conclusion

LGB continues to believe that laddered portfolios of bonds, ranging from gilts and T-Bills to MTNs, are an appropriate way to invest for income. Whereas until recently the rates offered on government-backed debt were negligible, they now offer greater potential. We continue to scan the AIM market for interesting longer-term opportunities, conscious that investors need to assume that they will get more than one bite of the investing cherry, so not to overcommit at the first opportunity, and that not all companies will succeed- but that at least EIS and related reliefs provide a degree of protection. We feel ETFs and Index Funds are the most appropriate ways of gaining exposure to major markets. Investment Trusts and other closed-end funds can be useful for gaining exposure to specific niche areas- and at the moment many are trading at very large discounts to their underlying asset value, a recurring problem for the sector, but also potentially an opportunity as discounts are closed.

Wherever you do invest we wish you all the best for 2024.

Transaction Manager

Alexia Rottet joined LGB in October 2025 as a Transaction Manager. Prior to LGB, she gained real estate experience by participating in the valuation of a property portfolio for A2immo.ch SA as a financial analyst, as well as working at Form Structural Design as an office manager. Alexia holds an MA in Entrepreneurship and Innovation and a BA in International Relations.

Relationship Manager

Ruby joined LGB in December 2024 as an Assistant Relationship Manager for our investing clients. She is responsible for all day-to-day transactions with investment clients and oversees the LGB Investments Platform and Deal Hub. Prior to LGB, Ruby worked at FHIRST, a start-up where she collaborated with the co-founders on revenue growth and improving client experiences. Ruby graduated with a First-Class degree in History from Durham University, and has obtained the CISI Level 4 Diploma in Investment Advice.

Finance Manager

Following a degree reading Chemistry at The Queen’s College, Oxford, Antonia trained to become a chartered accountant at a London-based audit firm. She then moved into the tax sector joining EY and completing the chartered tax adviser qualification. She then gained further experience working as a finance director within industry at a family office / hedge fund.

Programme size: £20m

Establishment Date: December 2017

Number of issues: 12

Sector: Marine tracking

Focus: Maritime surveillance and management

Programme size: £25m

Establishment Date: XX 2017

Number of issues: 20

Sector: Financial services

Focus: Loans and leasing

Associate Director

Omar joined LGB in February 2026 as an Associate Director in the Capital Markets team. He brings over five years of experience from NatWest, where he worked across the Leveraged Finance Origination and Portfolio Management teams. During this time, he supported a broad range of businesses from venture-backed to large-cap companies, with a primary focus on the mid-market. His experience was sector agnostic, and the majority of the companies he worked with were sponsor-backed, giving him extensive exposure to private equity-led transactions and capital structures. Omar holds a degree in Accounting and Finance from The London School of Economics & Political Science and is a Chartered Banker.

Adviser

Charles has played an important role in developing LGB & Co.’s investment approach by encouraging a focus on investing in businesses with strong IP or know-how with recurring revenue business models that can prosper throughout economic cycles. Charles brings over 30 years’ experience of investing in privately-owned and publicly-listed small and mid-market companies. He is a director of Larpent Newton & Co. and Hygea VCT plc. Charles qualified as a Chartered Accountant at Peat Marwick, now part of KPMG.

Adviser

Lisa has worked with LGB since 2015 in supporting the on-going cultural and organisational development of the firm, providing advice on strategic people matters. Since 2006, Lisa has been running her own consultancy and executive coaching business, People Possibilities Ltd. Her work is focused on supporting clients at an organisational, team and individual level to enable high performance,improve leadership capability and effect cultural and behavioural change. Previously Lisa has held senior HR leadership positions with Schroders, ABN AMRO and HSBC. Lisa graduated from the University of Birmingham with an honours degree in International Relations & French. She is a Fellow of the Chartered Institute of Personnel and Development (CIPD) and a qualified Executive Coach.

Chairman

Simon became non-executive Chairman of the Board of LGB & Co. with a focus on growth and strategic initiatives in December 2025. Simon has extensive experience in capital markets and wealth management. He previously ran the client and investment business of Heartwood and became Chief Executive in 2008. He led its well-regarded acquisition by Handelsbanken in 2013. Simon subsequently became NED and Chair of AIM-listed WH Ireland Group PLC. He was also asked to represent the wealth management sector on the FCA Smaller Business Practitioner Panel from 2013-2016.

Associate Director

Megan joined LGB in 2021 as a Relationship Manager. She is responsible for all day-to-day transactions with investment clients and oversees the LGB Investments Platform and Deal Hub. Prior to LGB, Megan worked at Puma Investments, a tax-efficient investment provider, in the sales and investor services team. Megan graduated from the University of Bath with a Bachelor of Science degree in Psychology, and has obtained the CISI Level 4 Diploma in Investment Advice.

Managing Director

Simone joined LGB in 2012 and is responsible for LGB & Co.’s business with institutional investors, wealth managers and sophisticated private investors. Simone’s team provides access to a range of compelling investment opportunities with a particular emphasis on structuring laddered portfolios of fixed income. In addition, the team manages portfolios of clients who have entered into advisory agreements with LGB Investments, and advises the fund managers of the Guernsey-based LGB SME Private Debt Fund. Prior to joining LGB & Co., Simone worked in the institutional fixed income department of Citigroup Global Markets. She began her career at Citigroup Private Bank in Geneva. Simone graduated from the University of Lausanne with a degree in HEC, Business Administration. She is a Chartered Member of the Chartered Institute for Securities & Investments and a Director of LGB.

CEO

Cedric was appointed CEO in July 2022 after a period of 18 months as a COO. Cedric spent 15 years working on the energy and commodities sales and trading desks for global banks (BNP Paribas, BAML and MUFG). He gained extensive international exposure, being based in London and Singapore and covering transactions in all geographic regions. Cedric graduated from Global Executive MBA at INSEAD in 2018 and started working in the capital markets space for growth-stage companies. He is also a director of LGB.

Managing Director, Capital Markets

Andrew founded LGB & Co. in 2005 and is managing the Capital Markets team. He has a particular focus on the development of strategic relationships with corporate clients and business partners. Prior to founding LGB & Co., Andrew was a Managing Director at Citigroup Global Markets, where he was responsible for its fixed-income business with private banks and retail institutions. Earlier in his career Andrew worked at Schroders in London and Tokyo. Andrew graduated from Oxford University with a degree in Modern History. He is a chartered member of the Chartered Institute for Securities & Investment.